1. Introduction

Globalization has caused dramatic pressures on countries in terms of obtaining comparative advan- tages in the global economy. Over the last fifty years, declining trade barriers and promoting foreign di- rect investment (FDI) have changed firms’ competitive strategies. In the globalized world economy, firms find alternative ways to reduce costs, increase productivity, capture competitiveness, and improve the management process (Maziarczyk, 2020). In this regard, international outsourcing is a well-known and widespread strategy for firms to achieve these goals. Particularly, liberalizing world trade and invest- ment through reducing taxes and promoting international financial flow has increased the strategic role of international outsourcing (Chadee and Raman, 2009). Hence, along with globalization, countries are integrated through different sectors to provide the cheapest raw materials, intermediate goods, and fin- ished products (Ikumapayi et al., 2020). As also called offshoring or fragmentation of production, inter- national outsourcing means that a firm in one country supplies the required raw materials, intermediate goods, manufactured goods, and services from outside the home countries (Molnar, et al., 2007; Choi and Yu, 2019). In the relevant literature, outsourcing (particularly international outsourcing) and offshoring are generally used interchangeably. However, there are some differences between the concepts of the two terms. Outsourcing can either take place domestically or internationally. Namely, firms can provide goods and services from inside a country’s borders (domestic outsourcing) or outside a country’s bor- ders (international outsourcing). Nevertheless, offshoring can occur from affiliates of domestic parent companies or independent providers (Bottini et al., 2007).

Although outsourcing is not a new phenomenon, thanks to globalization international outsourcing is still one of the most promising strategies to become more competitive in the international market. The positive influence of international outsourcing is not limited to cost reduction, but also transferring know-how, accessing modern technology, and learning management strategies are core benefits of firms in a globalization era (Johansson and Reischl, 2009). The term outsourcing emerged and has become widespread in the 1980s. It was first implemented through transferring non-essential functions based on sub-contracts or buying goods and services produced by external firms, called outsourcers, for de- manding firms, called outsourcees (Bilan et al., 2017). As argued by Grossman and Helpman (2002), out- sourcing covers different activities including product design, research & development (R&D), marketing, sales, distribution, and even after-sales services. Moreover, they asserted that outsourcing encompasses a broader scope than merely providing raw materials and intermediate goods. It means the establish- ment of a particular bilateral relationship with firms that undertake specific functions and make specific investments between firms.

Theoretically, the outsourcing strategy is closely related to global value chains (GVCs). Nowadays, GVCs are one of the main ways of producing and marketing goods. Firms involved in GVCs are gener- ally located in different countries, with each firm having a comparative advantage in various parts of commodities. Leading firms organize the GVCs and allocate the duties for partner firms to produce goods simultaneously. Typically, the production process of the iPhone can be easily understood in terms of the operation of the GVCs. The American firm Apple is leading in the value chain and specializes in several pro- cesses, including R&D and design of the models. However, Apple supplies the required components of the iPhone from different countries. Eventually, the production of the iPhone is realized in different countries and locations. Hence, the production is fragmentated with the GVC and becomes more sophisticated (Xing, 2022). According to the OECD, the GVCs account for around 85% of international trade (Chen and Shen, 2021). To participate in GVCs, multinational enterprises (MNEs) adopt outsourcing in various sectors. As an externalisation of value-adding to partners, outsourcing reflects the organisational fragmentation strategy of dominant firms, which manage the entire production process by allocating tasks to different firms. From this point of view, firms may tend towards outsourcing for different reasons. For example, reducing cost, technological development, and overcoming the skilled labour shortage (Chalaby, 2019).

Dizzying development in information technology and transportation costs have opened new possi- bilities to get goods and services from abroad at lower costs (Olsen, 2006). Classical international trade theories emphasize that a firm imports raw materials, intermediate inputs, or services from foreign providers where countries have a comparative advantage. Therefore, the benefits of international out- sourcing occur in case comparative advantage exceeds the cost of outsourcing (Swenson and Chen, 2018). International outsourcing has adopted predominantly developed countries such as the European Union (EU) and United States (US), and they supply substantial amounts of parts of goods and services from developing countries (Choi and Yu, 2019). In most phases of the 20th century, outsourcing was composed mainly automotive industry. However, the general pattern of outsourcing has changed and shifted to technological tools since the 1980s (Zulaykho et al., 2022). Besides, along with the internation- alization of production, outsourcing destinations vary in the global economy. Nowadays, China and India are two leading important international outsourcing destinations. According to the UNCTAD (2023), a tremendous rise in exports and import have occurred in both two countries. China’s export was around 18 billion US dollars in 1980; it reached 3.6 trillion US dollars in 2022. The Chinese government has im- plemented different policies to integrate into the world economy. After the economic reform initiated in 1978, China liberalized its trade structure, and the export-led growth model characterized the Chinese economy. During this process, the Chinese economy was not only dependent on exports of primary com- modities production. Also, high-tech industrial zones have been composed to upgrade exportable goods (Gozgor and Can, 2017). China’s integration into the world economy has contributed to an increase in international trade. As a result, both exports and imports have grown faster than the global economy in the last decades. The economic reform that was initiated in 1978, aiming for trade and investment liber- alization of the Chinese economy, and accession to the World Trade Organization (WTO) in 2001 caused significant reductions in import tariffs and contributed to import growth. China’s increasing role in in- ternational trade is crucial for regional trade in Asia. Outsourcing has become a vital strategy to extend bilateral trade flows, leading to increased imports of China from within the region. Thus, China became the leading export destination for Asian countries (Rumbaugh and Blancher, 2004).

China’s import has risen dramatically from 1980-2022. For example, China’s import has increased from 20 billion US dollars in 1980 to 2.7 trillion US dollars in 2022. Intermediate goods are China’s largest import category, as statistical data shows that China’s 70% of its imports comprise intermediate goods (Xiang et al., 2022). India has also experienced remarkable trade growth since the 1980s. The export volume was around 8.5 billion US dollars in 1980 and increased to 453.5 billion US dollars in 2022. Simi- larly, the sharp rise in imports stands out in India. The import volume has increased from 14.9 billion US dollars in 1980 to 723.4 US dollars in 2022. Until 1990, the Indian markets were protected with high-lev- el tariffs and non-tariff barriers. However, after 1991, the Indian industry facilitated trade barriers in the import of intermediate and final goods. As a result, the average tariff rate declined from 86.82% to 14.57% from 1990-2009. In addition, the non-tariff barrier coverage ratio declined from around 100% to 0% in the same period (Mukherjee and Chanda, 2019). Opening its markets to international competition has promoted access to new input varieties for Indian firms from overseas (Goldberg et al., 2009).

Generally, China and India are labeled as the “world’s factories.” It is a fact that both countries have grown by producing cheaper and with relatively lower costs than in many other countries, and export had a vital role in sustainable economic growth in China and India. Therefore, the mainstream view tends to concentrate on the export performance of China and India. However, international outsourcing in China and India is ignored in the relevant literature. In other words, it is crucial to determine the share of foreign suppliers in imports from these countries. To fulfill the gap in existing literature, this paper aims to investigate international outsourcing in China and India in total economy and different sectors, including industry, agriculture, manufacturing, services, and technology, by employing annual data cov- ering 1995, 2008, 2009, and 2018 obtained from input-output data.

Our study focuses on China and India due to some reasons: Firstly, China and India have achieved re- markable trade growth during the last two decades. Although the export-led growth model has triggered their development path, it is crucial to determine outsourcing for these countries. Secondly, the import volume index has risen from 10.3 to 647.1 from 1980-2020 in China and from 21.5 to 508.3 in the same period in India. Thus, examining international outsourcing for China and India would be appropriate (World Bank, 2023). The contributions of the present study are two folds. Firstly, to the best of our knowl- edge, this study provides the first systematic and detailed comparison of China and India using the latest OECD GCT tables (1995-2018) and ISIC Rev.4 classifications covering 45 sub-sectors. By applying both the broad and narrow definitions of outsourcing, it offers a comprehensive assessment of cross-country frag- mentation patterns. It is also the first study to examine outsourcing across manufacturing sub-sectors grouped by technological intensity (e.g., high-technology, medium-low-technology). This dual-definition and technology-based approach generates novel insights into the two countries’ positions within GVCs.

The paper is organized into the following sections: Section 2 covers the literature review. Section 3 outlines the methodology. Section 4 reports the findings, and Section 5 presents the conclusion and policy implications.

2. Literature review

The literature on international outsourcing has expanded rapidly, reflecting its transformative role in global business operations and sectoral dynamics across manufacturing, services, information and communication technology (ICT), and automotive industries. Outsourcing is broadly defined as the sourcing of inputs from foreign independent suppliers. Initially concentrated in manufacturing since the 1980s, international outsourcing has since expanded to include services and advanced knowledge activ- ities such as research and development (R&D) and design. Prominent examples include Apple’s iPhone production subcontracted to China and ABN-AMRO outsourcing IT services to IBM (Lee and Mol, 2024). The economic effects of international outsourcing are multifaceted. Feenstra and Hanson (1999) examined the influence of trade and technology on wages, revealing that while computers accounted for roughly 35% of wage increases among non-production workers, outsourcing explained around 15%. Similarly, Mukherjee and Tsai (2010) warn that outsourcing may reduce domestic welfare, emphasizing the strategic importance of such decisions for firms. Hashimoto (2010) highlighted the roles of exchange rates and effective demand in shaping labor demand within global production networks. Empirical ev- idence points to productivity gains as a key benefit of outsourcing, especially in labor-intensive sectors (Bandopadhyay et al., 2014). However, outsourcing’s effects on labor markets vary by skill level; Hijzen (2005) noted that unskilled workers tend to bear the brunt of negative impacts, while Geishecker and Görg (2008) documented wage declines up to 1.5% for low-skilled workers alongside wage gains up to 2.6% for high-skilled workers. Lahiri et al., (2022), through a meta-analysis of over 100 studies, found that outsourcing generally improves firm performance, particularly for non-core activities and interna- tional sourcing, with effects consistent across manufacturing and services. Operational risks inherent in outsourcing are also recognized. Uygun et al., (2023) identified challenges such as innovation traps, bargaining power shifts, plagiarism, and knowledge loss. The management of outsourcing relationships is critical, as cost and quality criteria significantly affect partnership integration (Kaipia and Turkulain- en, 2017). Maelah et al., (2010) found that the risk of dependency on foreign suppliers and the potential for service quality degradation are significant concerns that firms must address when implementing outsourcing strategies. Moreover, Hsu and Chiang (2014) discussed the potential for increased wage disparities in labor markets due to outsourcing. Hijzen et al., (2010) examine the impact of offshoring on firm productivity utilizing data from Japanese firms spanning the period from 1994 to 2000. The findings suggest that offshoring generally has a positive effect on productivity growth, and this effect remains robust even when accounting for the potential endogeneity of offshoring concerning unobserved produc- tivity shocks.

Outsourcing impacts differ markedly across sectors. Egger and Egger (2006) showed that outsourc- ing initially reduces real value added per low-skilled worker in the European Union but benefits accrue in the long term. Aubuchon et al., (2012) found outsourcing more prevalent in German manufacturing than services, with outsourcing intensity positively correlated with plant-level productivity. Gencer (2022) confirmed a steady rise in outsourcing in Türkiye’s manufacturing sector. Amighini (2012) highlighted the distinct roles of China and India in automotive global value chains (GVCs), with China as a net im- porter of cars and India as a net exporter, both increasingly involved in vertical labor division. Bachmann and Braun (2011) observed that outsourcing tends to improve job stability in services, contrasting with mixed results in manufacturing. Park (2024) revealed that U.S. service offshoring to India reduced total employment from 2000 to 2006 but generated positive employment effects for college-educated work- ers thereafter. Ye and Yan (2024) demonstrated that service outsourcing generally boosts labor income shares, though offshore outsourcing in China correlates with lower labor shares. Kite (2012) found ICT outsourcing in India positively affects both output and productivity. Wang et al., (2025) showed that digital technologies, including AI and robotics, enhance the tradability of services across 76 economies, driven by labor shifts and economies of scale. Duan et al., (2018) documented China’s vertical special- ization rising until 2004, followed by a decline linked to substitution of imported intermediates with domestic products. Chen and Shen (2021) emphasized offshore outsourcing’s role in advancing China’s manufacturing and services sectors within GVCs, facilitated by factors like human capital and the com- mand economy.

Recent studies highlight shifts in global outsourcing dynamics. Nartey (2025) identifies a struc- tural reshoring trend in Western countries driven by automation, robotics, and AI, fueled by pandemic disruptions and geopolitical tensions. This movement challenges traditional comparative advantage the- ories and risks premature deindustrialization in developing nations. Song et al., (2025) analyze China’s Offshore Service Outsourcing (OSO) under floating exchange rates, finding that Information Technology Outsourcing dominates, supported by emerging privacy-preserving computing technologies. Di Berardi- no et al., (2025) challenge narratives of deindustrialization in Europe, showing stable or growing man- ufacturing employment, driven by exports to non-European markets and deeper integration of services and manufacturing value chains. Environmental considerations are increasingly relevant; Kar and Ba- nerjee (2022) found that higher pollution abatement costs in India encourage outsourcing, though this is moderated by energy prices and firm profitability. Thakur-Wernz and Wernz (2022) showed that Indian biopharmaceutical firms engaged in R&D offshore outsourcing outperform peers in innovation, under- scoring the importance of technological capabilities and client-driven learning.

In conclusion, international outsourcing continues to offer substantial opportunities for produc- tivity enhancement, innovation, and economic efficiency. Nonetheless, it also presents challenges such as labor market disruptions, wage disparities, and strategic risks. Effective management of cross-bor- der relationships and an understanding of sector-specific and regional contexts are essential. Future research should deepen exploration of outsourcing’s nuanced impacts, particularly for small- and medium-sized enterprises and emerging economies, while considering evolving technological and geo- political developments.

3. Materials and Methods

International outsourcing, defined as the use of external resources (Mishina et al., 2019), refers to the procurement of activities carried out within a sector in the form of semi-finished products, finished products, or services from foreign companies (Dolgui & Proth, 2013). In other words, domestic firms engage in outsourcing to foreign suppliers in order to benefit from lower labor costs and intermediate inputs available abroad (Ho, 2021). This also shows the use of imported inputs in the production process- es of the sectors. In this context, the primary aim of the study is to examine, using existing data, the pat- terns of international outsourcing at both the aggregate and sectoral levels in two major global trading powers – China and India. In order to analyze outsourcing in the economies of China and India, national Input-Output Tables from the OECD database for 1995-2018 are used. These tables, prepared according to ISIC Rev.4, consist of 45 sub-sectors, 17 of which are manufacturing industry sub-sectors. Input–Out- put Tables are constructed for specific reference periods and entail substantial temporal intervals. The Input–Output Tables utilized in the present study were prepared by the OECD (2021) and encompass the period from 1995 to 2018. To analyze outsourcing, studies by Feenstra and Hanson (1999), Horgos (2009), Hijzen et al., (2005), Hijzen (2007), and Geishecker (2007) are considered as references. Four different indexes are used in the literature to measure outsourcing. These indexes are, Imported Inputs in Total Inputs (IITI), Imported Inputs in Gross Output (IIGO), Imported Inputs in Total Imports (IITM), and Imported Input in Value Added (IIVA), respectively (Horgos, 2009: 613). All of these indexes funda- mentally measure the import dependency of a country or a specific sector. However, there are specific differences among these indexes. For example, the IITI index measures the share of imported intermedi- ate inputs in the total intermediate inputs utilized within a country’s or sector’s production process. The IIGO index indicates the proportion of imported intermediate inputs used in a country or sector’s gross output in a given year. The IITM index indicates the proportion of imported intermediate inputs within a country or sector’s total imports during a given year. Finally, the IIVA index represents the proportion of value-added derived from imported inputs within a country or sector during a given year.

Further, outsourcing in sub-sectors of the manufacturing industry for technology (in Tables 1 and 2) is calculated for 1995, 2008, 2009, and 2018. The indexes mentioned above are calculated as follows:

Table 1

International outsourcing in sub-sectors of manufacturing in China (IITI index)2

Table 2

International outsourcing in sub-sectors of manufacturing in India (IITI index)

i) Imported Inputs in Total Inputs (IITI)

In Eq. [1], iwjt denotes the intermediate input imported from sector w (w = 1, …, z) to produce output in sector j (j = 1, …, n) in year of t, qwjt denotes the total intermediate input required to produce output in sector j (j = 1, …, n) in a given year. Total intermediate input (qwjt) is the sum of domestic intermediate (dwjt) and imported intermediate input (iwjt) (Geishecker and Görg, 2005: 85-86; Cadarso et al., 2008: 100-101). The adaptation of this index to Input-Output Tables is employed through using the following formula (Gencer, 2022: 78; Horgos, 2008; Aubuchon et al., 2012: 292):

In Eq. [2], i denotes the nx1 vector of the imported intermediate inputs, d indicates the nx1 domestic vector of intermediate inputs, q indicates the nx1 vector of total intermediate, and

ii) Imported Inputs in Gross Output (IIGO)

In Eq. [3], iwjt indicates the imported intermediate input from sector w (w = 1, …, z) to produce output in sector j (j = 1, …, n) in year of t. In this equation, Owjt is the gross output in year of t. The adaptation of the IIGO index to input-output tables is employed with the following formula (Geishecker, 2007: 4-6; Horgos, 2009: 613-614; Bachmann and Braun, 2011: 8-9):

In Eq. [4], i denotes the nx1 vector of the imported intermediate inputs, o denotes the nx1 gross out- put of the sector and

iii) Imported Inputs in Total Imports (IITM)

In Eq. [5], iwjt is the imported intermediate input from sector w (w = 1, …, z) to produce output in sector j (j = 1, …, n) in year of t and mwt is the total value of imports. The adaptation of the IITM index to input-output tables is employed with the following formula (Horgos, 2008: 9-10; Horgos, 2009: 613):

In Eq. [6], i denotes the nx1 vector of the imported intermediate inputs, m denotes the nx1 total im- port vector of the sector and

iv) Imported Input in Value Added (IIVA)

In Eq. [7], iwjt is the imported intermediate input from sector w (w = 1, …, z) to produce output in sector j (j = 1, …, n) in year t and vwt is the value added, i.e., basic inputs. The adaptation of the IIVA index to input-output tables is employed with the following formula (Hijzen et al., 2005: 864-865; Hijzen, 2005: 50-51):

In Eq. [8], i denotes the nx1 vector of the imported intermediate inputs, v denotes the nx1 vector val- ue added of the sector and

4. Results and Discussions

Building on the approaches of Feenstra and Hanson (1999), Hoger (2009), Amiti and Wei (2005), and this study investigates the extent of international outsourcing in the Chinese and Indian economies. These countries – emerging as major trading powers in the post-1980 era of neo-liberal reforms – are examined at both the sectoral and manufacturing sub-sector levels. The analysis quantifies international outsourcing, in both its narrow and broad definitions, using the IITI index as one of four measurement indices. In the narrow sense, outsourcing only considers intermediate inputs imported from the same industry. On the other hand, on a broad scale, sectoral intermediate input imports include the imports of intermediate inputs produced within the same industry and the input imports obtained from all indus- tries without restrictions, which are used to produce the final goods and services. Therefore, it can be said that the broad measurement better reflects outsourcing (Gencer, 2022: 3-7). The reason for choosing this index is that it is widely used in the literature. The findings obtained for outsourcing by calculating the IITI index are presented in Figure 1, Figure 2, Figure 3, Figure 4, Table 1, and Table 2.

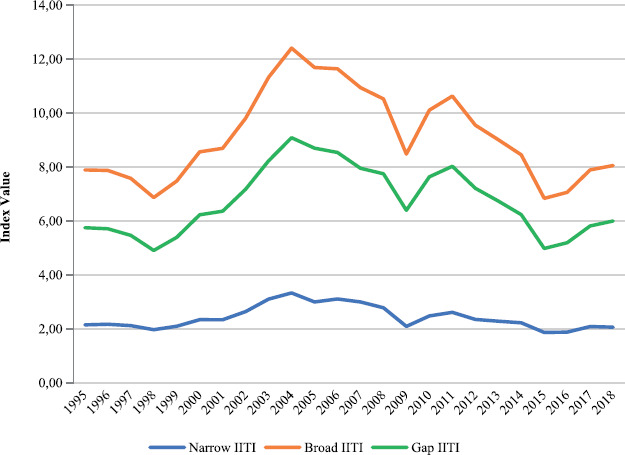

Figure 1

International outsourcing in China (IITI index) for total economy, 1995-2018

Source: authors’ own calculations.

Figure 2

International outsourcing in China (IITI index) for sub-Sectors, 1995-2018

Source: authors’ own calculations.

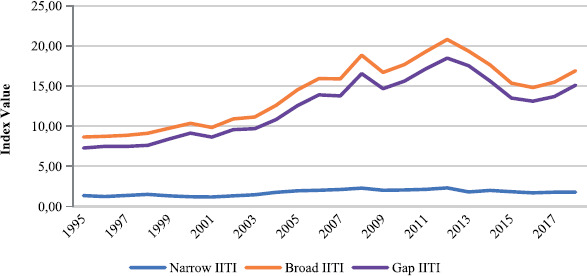

Figure 3

International outsourcing in India (IITI index) for total economy, 1995-2018

Source: authors’ own calculations.

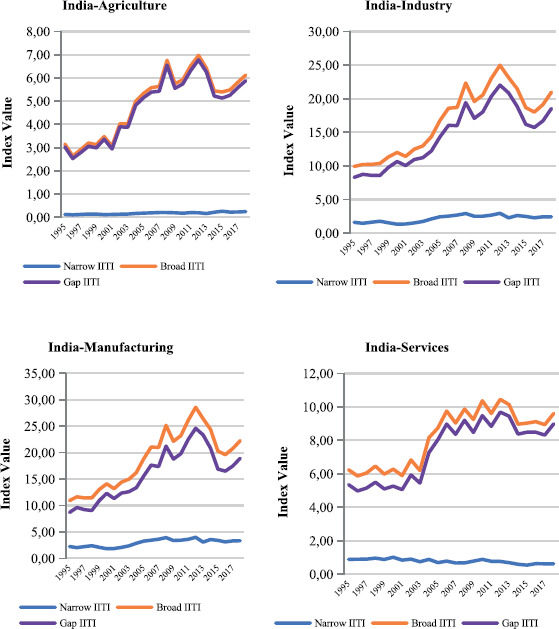

Figure 4

International outsourcing in India (IITI index) for sub-sectors, 1995-2018.

Source: authors’ own calculations.

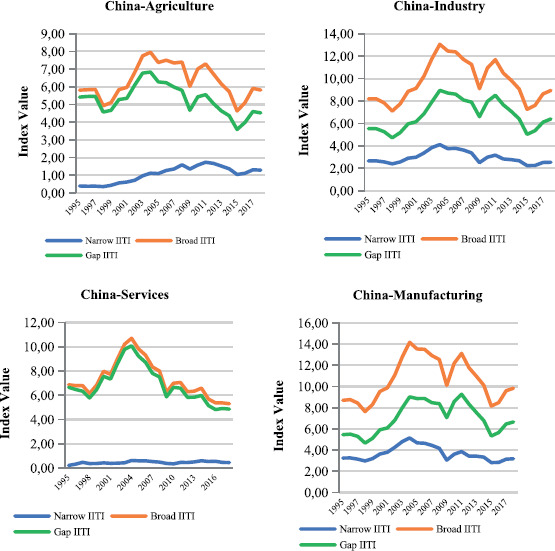

Figures 1 and 2 show the international outsourcing tendency of China’s total economy and main sub-sectors. International outsourcing has shown a significant increase in both the overall economy and the main sub-sectors until 2004. However, after 2004, international outsourcing tended to decrease. The manufacturing industry was the largest international outsourcing sector in 2004. The decline in international outsourcing continued until 2009. It increased between 2009-2011 and decreased between 2011-2015. However, since 2015, international outsourcing has increased almost in the overall economy and the main sub-sectors. The manufacturing industry was the largest international outsourcing sector in 2018, with a 9.6 index value; service was the lowest international outsourcing in 2018, with a 5.30 index value. As shown in Figures 1 and 2, the extent of broad international outsourcing in the Chinese economy – both at the aggregate level and across the main sectors – exceeds that of narrow international outsourcing. Accordingly, the broad IITI index is greater than its narrow counterpart. This suggests that sectors, in expanding their use of imported inputs, source not only intermediate goods produced within their own sector group but also intermediate inputs from a wide range of other sectors for the production of final goods (Gencer, 2022).

Figures 3 and 4 depict the international outsourcing trends of India’s total economy and its main sub-sectors. In the Indian economy, international outsourcing increased steadily until 2008, with the exception of the services sector. Between 2009 and 2013, outsourcing levels rose, followed by a decline from 2013 to 2016, after which they began to rise again. In the services sector, outsourcing remained relatively stable until 2003, decreased in 2004, and thereafter exhibited a trend distinct from other sec- tors, as illustrated in Figure 4. In 2018, the manufacturing industry recorded the highest international outsourcing index value at 22.3, while agriculture registered the lowest at 6.13. Similar to the case of China, narrow international outsourcing in India is lower than broad international outsourcing. This in- dicates that Indian sectors, in expanding their use of imported inputs, source not only intermediate goods produced within the same sectoral group but also intermediate inputs from a wide range of sectors for the production of final goods (Gencer, 2022).

Table 1 shows international outsourcing in sub-sectors of China’s manufacturing industry. As de- picted in Table 1, the computer, electronic, and optical equipment (26) sector has the highest level of international outsourcing in the narrow sense in all periods in China’s manufacturing industry. However, the non-metallic mineral products (23) sector had the lowest level of international outsourcing in 1995 and 2009, and manufacturing nec; repair and installation of machinery and equipment (31T33) had the lowest level of international outsourcing in 2008 and 2018 in narrow terms.

In broad terms, the computer, electronic, and optical equipment (26) sector only had the highest international outsourcing level in 1995. In contrast, the coke and refined petroleum products (19) sector was the highest international outsourcing for the rest of the period. In contrast, pharmaceuticals, me- dicinal chemical, and botanical products (21) in 1995, food products, beverages, and tobacco (10T12) in 2008 and 2018, and the textiles, textile products, leather, and footwear (13T15) sector in 2009 had the lowest international outsourcing in a broad sense.

According to the technological classification, the high-tech sector recorded the highest international outsourcing index values – both in narrow and broad terms – throughout all periods. For instance, in narrow terms, the index stood at 10.23 in 1995, 17.13 in 2008, 11.82 in 2009, and 11.67 in 2018; in broad terms, the corresponding values were 15.05, 23.37, 16.59, and 15.76, respectively. By contrast, the medi- um-low-tech and low-tech sectors consistently exhibited the lowest levels of international outsourcing in narrow terms, with values of 0.47 (1995), 0.26 (2008), 0.28 (2009), and 0.16 (2018). In broad terms, the medium-low-tech sector recorded the lowest level in 1995 (7.62), whereas the low-tech sector had the lowest levels in subsequent years – 5.88 in 2008, 4.82 in 2009, and 4.53 in 2018.

Table 2 shows international outsourcing in sub-sectors of India’s manufacturing industry. In a nar- row sense, the sub-sectors with the highest-level international outsourcing in the Indian manufacturing industry are as follows: chemical and chemical products (20) in 1995, other transport equipment (30) in 2008, and manufacturing n.e.c; repair and installation of machinery and equipment (31T33) in 2009 and 2018. In a narrow sense, the sector with the lowest level of international outsourcing is food products, beverages, and tobacco (10T12) in 1995, 2008, and 2009, and the motor vehicles, trailers, and semi-trail- ers (29) sector in 2018.

In a broad sense, the sub-sectors with the highest level of international outsourcing are as follows: computer, electronic, and optical equipment (26) in 1995 and coke and refined petroleum products (19) in 2008, 2009, and 2018. In a broad sense, the sector with the lowest level of international outsourcing is the food products, beverages, and tobacco (10T12) sub-sector in all years.

The technological classification results reveal important structural differences between China and India that carry clear implications within the broader theoretical frameworks of global value chain (GVC) integration, fragmentation theory, and the literature on upgrading. In the narrow definition, China’s me- dium-high-technology manufacturing sector recorded the highest international outsourcing intensity in 1995 (4.52), whereas the medium-low-technology segment dominated thereafter (reaching 13.13 in 2008, 16.16 in 2009, and 14.79 in 2018). Low-technology industries consistently exhibited the lowest outsourcing levels throughout the period. Under the broad definition, the medium-low-technology sector maintained the highest outsourcing intensity across all years, rising sharply after the 2000s. Low-tech- nology industries again remained the least integrated through imported intermediates.

These patterns underscore an important theoretical implication: both China and India rely not only on within-industry imported intermediates (narrow outsourcing) but increasingly on cross-industry input sourcing (broad outsourcing), confirming the predictions of fragmentation theory (Jones & Ki- erzkowski) and multi-sectoral GVC models. The dominance of broad outsourcing suggests that manu- facturing production in both economies is embedded in wide supplier networks that extend far beyond their core industry boundaries. This structural feature is associated with deeper GVC participation and, theoretically, with opportunities for process upgrading but also with heightened exposure to external shocks.

A deeper interpretation of China’s outsourcing trajectory reveals distinct phases that correspond closely with its policy shifts and theoretical expectations regarding domestic value creation, localisation, and GVC rebalancing. The rapid increase observed between 1998 and 2004 aligns with China’s WTO accession and its integration into vertically fragmented production networks, consistent with the litera- ture emphasising the role of trade liberalisation in lowering service-link costs and accelerating interna- tional fragmentation. However, the decline after 2004 reflects China’s gradual transition from an assem- bly-based, export-driven model toward higher domestic value retention, in line with the “Made in China” upgrading policies. As China moved up the value chain, it deliberately pursued localisation strategies, import substitution in key intermediate inputs, and technological self-sufficiency policies – trends that economic theory associates with functional upgrading, wherein countries internalise more high-value tasks previously sourced from abroad. Thus, the post-2004 decline does not necessarily indicate reduced global integration; rather, it signals a shift toward deeper domestic capability formation and a more do- mestically anchored supply chain structure.

India’s pattern differs substantially and is more consistent with a late-industrialisation model where rising outsourcing reflects integration into GVCs through intermediate input trade. The steady increase in India’s outsourcing intensity – particularly in medium-technology manufacturing – can be interpreted through Lall’s technological capability framework and the “flying geese” model. India has relied exten- sively on imported intermediates to compensate for domestic technological gaps, facilitating process up- grading without immediate domestic value creation. This pattern results in higher intra-industry trade intensity (IITI) in manufacturing, signalling India’s expanding role in modularised production networks. Unlike China, India’s industrial policy has placed less emphasis on large-scale localisation until more recent initiatives such as “Make in India,” and thus its rising outsourcing does not reflect functional up- grading but rather continued external dependency characteristic of a middle-stage GVC participant. The temporary declines during 2008-2009 and 2012-2016 coincide with the global financial crisis and domes- tic demand contractions, consistent with theoretical expectations that countries with higher reliance on imported intermediates experience more pronounced cyclical sensitivity.

Overall, the findings confirm that international outsourcing is higher in manufacturing than in agri- culture or services for both countries, but the interpretation of these levels differs significantly. In China, high outsourcing in high-technology industries is accompanied by a long-term trend toward domestic capability expansion and value capture. In India, higher outsourcing in medium-technology industries signals integration without substantial localisation. These contrasting dynamics align with existing em- pirical evidence (Aubuchon & Bandyopadhyay, 2012; Gencer, 2022; Amighini, 2012; Chen & Shen, 2021) while diverging from studies such as Dietzenbacher et al. (2018), which emphasise China’s continued import dependence.

Importantly, these results highlight that outsourcing intensity cannot be interpreted solely as a measure of integration; rather, its evolution must be examined alongside industrial policy, technological capability accumulation, domestic value-added strategies, and GVC upgrading paths. The declines ob- served in China after 2004 and the sustained rise in India’s manufacturing IITI illustrate two distinct development trajectories: one characterised by increasing localisation and domestic value creation, and the other by deeper integration accompanied by continued external technological dependence. This in- terpretation provides a richer economic context to the numerical findings and offers significant insights into how countries reposition themselves within global value chains over time.

5. Conclusion and Policy Recommendations

In the post-1980 period, the world economy has undergone a great transformation. Globalization is one of the essential driving forces of this transformation. In order to integrate with the global economy, countries have moved towards removing trade barriers, liberalizing trade, and adopting outward-orient- ed and export-oriented policies. In this context, China and India have undergone severe policy changes in the post-1980 period to integrate into the global economy.

In China, reforms began in 1978, and export-oriented and trade-liberalization policies were grad- ually implemented. Through these reforms, China emerged not only as a major global manufacturing base but also as the central anchor of Asian production networks. Its rapid integration into global value chains positioned China as the principal driver of East and Southeast Asian industrial upgrading. In India, by contrast, the domestic market was protected by high tariffs and non-tariff barriers until the 1990s. However, in the aftermath of the 1990s, the Indian economy took significant steps to integrate with the global economy by removing these tariffs and trade barriers. While India did not match China’s pace, it has become increasingly important within its own geographical context – particularly in South Asia and the Indian Ocean region – where its economic size, demographic structure, and expanding industrial base have strengthened its regional influence.

As a result of these policies, China and India have become important nodes within global production networks. Participation in the global production system has been facilitated by international outsourc- ing, which has become an essential strategy for expanding bilateral and multilateral trade flows. In this direction, the present study analyses international outsourcing for China and India by considering dif- ferent sectors. According to the findings, international outsourcing is higher in the industry/manufac- turing sector and lower in the service sector in China. International outsourcing in China has fluctuated constantly. It declined sharply, especially during the crisis periods (the 1997/1998 Asian crisis and the 2008/2009 global financial crisis). However, there has been an increasing trend after 2015. These fluctu- ations reflect China’s strategic shift toward domestic value creation, technology upgrading, and reducing vulnerability to global input dependency – developments particularly relevant given China’s central role in Asian value chains.

In India, the industry/manufacturing sector had the highest level of international outsourcing, and the agriculture sector had the lowest. International outsourcing increased almost continuously until the 2008/2009 global financial crisis. Although it slowed during this period, outsourcing began to rise again after 2016. India’s patterns indicate growing integration into regional and global production systems, particularly in sectors where imported intermediates compensate for domestic technological limitations. Thus, while China’s outsourcing pattern reflects a combination of deep GVC integration and subsequent localisation efforts, India’s increasing outsourcing levels mirror its progressive insertion into global pro- duction structures within its regional environment.

According to technological classification, high-tech sectors had the highest level of international outsourcing in China, whereas medium-high-tech and medium-low-tech sectors had the highest levels in India. Regarding the manufacturing industry’s sub-sectors, coke and refined petroleum products (19) had the highest level of international outsourcing in 2018 in both China and India. A high level of inter- national outsourcing means a high dependence on imported inputs in production.

Dependence on imported intermediate inputs may create certain disadvantages for economies. In particular, during periods of economic crisis, exchange rate depreciations may lead to rising production costs and, consequently, to inflation. This may increase the vulnerability of economies to external shocks. In the event of emerging geopolitical risks, domestic production may face severe bottlenecks. Moreover, in some cases, dependence on imported intermediate inputs may adversely affect the international com- petitiveness of developing countries. In this context, special consideration should be given to the use of external resources in technology-intensive sectors; alternatively, technological capabilities should be developed through learning-by-doing, while domestic production should be actively promoted. Ensuring the continuity of production during periods of crisis necessitates sustained investment in human capital and the accumulation of technological capabilities.

This study is subject to several limitations. Firstly, we focus on revealing the outsourcing level by in- vestigating Input–Output Tables. The Input–Output model relies on statistical data as its primary source, while its methodology is grounded in mathematical and economic modeling. To estimate the relationship between outsourcing and other variables, a long data set is required at the sectoral level. Hence, once data becomes available, research can be conducted to investigate the association between outsourcing and other variables using statistical methods. Secondly, we investigate outsourcing in China and India. Nowadays, there are various emerging economies in the world; future studies may also examine the out- sourcing level for other countries to compare themselves.